Delayed Energy Transition Could Mean Higher Hydrocarbon Prices

January 16, 2025

As the risk of a delayed energy transition scenario increases, so does the possibility of a much greater pull on future oil and gas supply, but meeting this demand would require a significant increase in upstream investment, resulting in higher hydrocarbon prices, according to the latest Horizons report from Wood Mackenzie.

According to the report “Taking the strain: how upstream could meet the demands of a delayed energy transition”, a variety of external pressures have weakened government and corporate resolve to spend the estimated $3.5 trillion required to restructure energy systems to limit both hydrocarbon demand and global warming.

The report focuses on the additional resources and spend required if the upstream sector was to meet higher-for-longer oil and gas demand, and the resultant consequences.

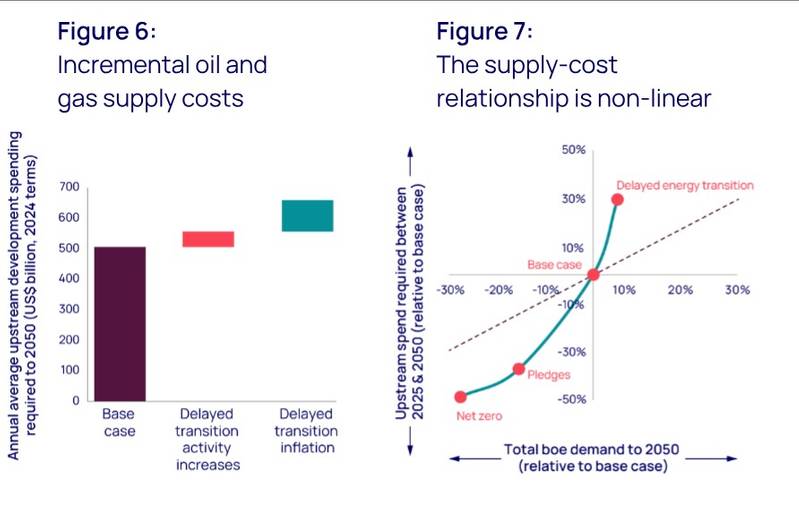

Under this scenario the world would require 5% more oil and gas supply and 30% higher annual upstream capital investment.

Plenty of supply is available to meet rising demand in the near term. “However, stronger-for-longer demand growth is a much stiffer ask. A five-year transition delay would require incremental volumes equivalent to a new US Permian basin for oil and a Haynesville Shale or Australia for gas,” said Angus Rodger, head of upstream analysis for Asia-Pacific and the Middle East.

While Rodger believes the global oil and gas sector could meet this demand through existing resources and future exploration, significant investment would be required to achieve it.

Wood Mackenzie estimates that upstream spending would have to rise by 30%, resulting in $659 billion of annual development spend versus $507 billion in the base case, and $17 trillion versus $13 trillion in total to 2050 (all in 2024 terms).

But increasing spend won’t be easy, even if the signs of increased demand are present. More activity would put significant pressure on the supply chain – parts of which are already running near capacity – and project costs would inflate.

“The industry’s current strict capital discipline edict would also have to change or, at least, what defines discipline would have to evolve,” said Rodger.

“Corporate planning prices would increase if the outlook for the market improved, with increased confidence in demand longevity. In that environment, higher development unit costs and breakevens would likely be tolerable,” said McKay.

With the higher cost of supply, so too would come higher prices for both oil and gas. Wood Mackenzie’s Oil Supply Model forecasts a Brent price rising to over $100/bbl during the 2030s in a delayed transition scenario. It falls towards $90/bbl by 2050, averaging around $20/bbl higher than the base case over the period (all in 2024 terms).