Global Offshore Wind Prospects to Rebound in 2025

March 4, 2025

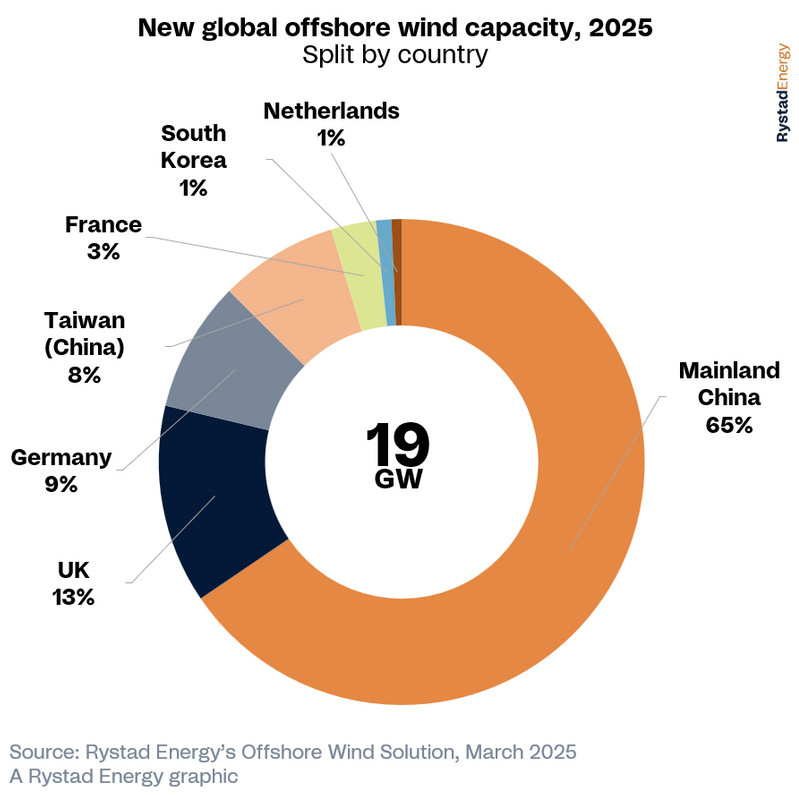

The global offshore wind industry is poised for a rebound in 2025, with capacity additions expected to reach 19GW and sector-wide expenditure projected to hit $80 billion, according to research from Rystad Energy.

This recovery follows a slowdown at the end of last year, when new installations dropped to approximately 8GW, which is 2GW lower than the year prior.

A record wave of lease auctions is driving the resurgence, with the world’s largest offshore wind market, mainland China, accounting for 65% of new capacity. With this increase, total additions will exceed the previous peak in 2021 by about 1GW, surpassing the 7.7GW added in 2024, 10.2GW in 2023 and 9.3GW in 2022.

A record 55GW of offshore wind capacity was offered in lease auctions globally (excluding mainland China) in 2024. However, not all this capacity has yet been awarded, as offered capacity does not always translate into awarded capacity. For instance, the US saw no bids for its 3GW floating wind auction in Oregon last year, while the Gulf of Maine auction awarded roughly 7GW of the approximately 13GW offered.

Despite 2024's record offerings, lease auction openings are projected to decline in 2025, with an expected 30-40GW available. While significantly lower than 2024, this projected offered capacity is still significant, aligned with levels seen in 2021 and 2022.

“Global offshore wind is set for a robust year in 2025. However, certain signals could affect its smooth upward trajectory. US federal policy is creating significant global ripple effects, hindering offshore wind development, especially where a large portion of auctioned capacity lies. President Donald Trump’s January memorandum halting new leasing and approvals on the Outer Continental Shelf (OCS), citing environmental and safety concerns, could last throughout his term, pausing new developments and creating continued uncertainty for ongoing projects," said Petra Manuel, Senior Offshore Wind Analyst, Rystad Energy.

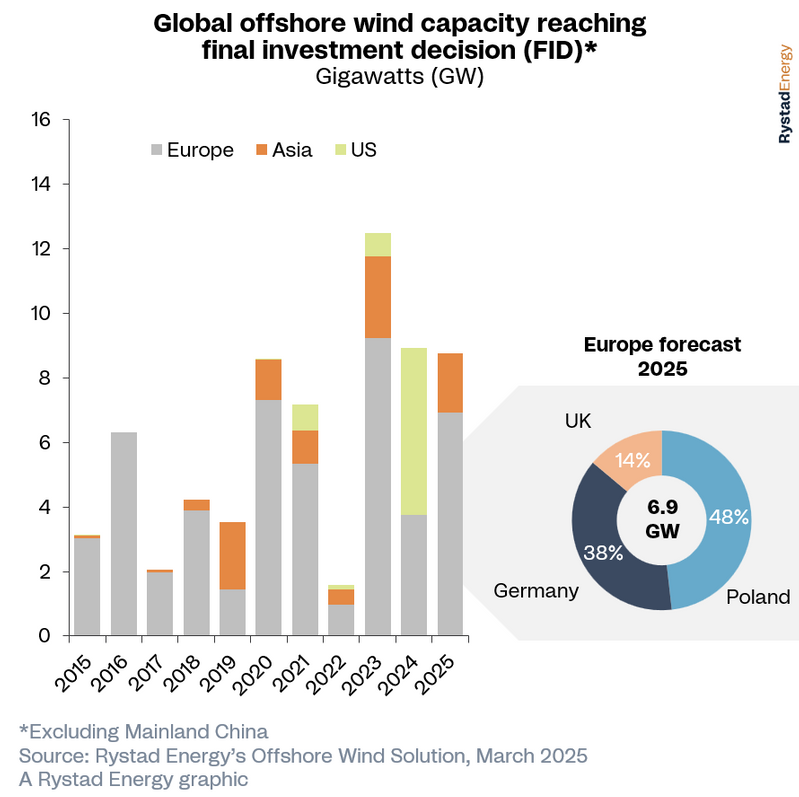

Project delays significantly impacted final investment decisions (FID) for new offshore wind projects in 2024, leading to a decline in project approvals. Notably, 2024 saw only a few US projects reach FID, including Empire Wind 1, Sunrise Wind and Costal Virginia Offshore Wind.

“We expect to see around the same level of FIDs this year as last in Europe and Asia, and some possible upside in the US with US Wind, Southcoast Wind and New England Wind projects obtaining offtake agreements and construction and operation approvals. The latter two just postponed signing offtake contracts until March this year.”

Despite the slow pace of sanctioning in 2024, the year developers advanced projects like Red Rock Power and ESB’s 1.1-GW Inch Cape in the UK and Equinor’s 810-MW Empire Wind 1 in the US. Inch Cape, which formally announced its financial close status in January 2025, secured 15-year contracts for difference (CFD) in both 2022 and 2024, providing revenue certainty and boosting investor confidence. Other wind farms reaching FID in 2024 include Iberdrola’s 315-MW Windanker in Germany, RWE and TotalEnergies’ 795-MW OranjeWind in the Netherlands, and Orsted’s 924-MW Sunrise Wind 1 in the US.

The UK, Poland and Germany are set to lead a surge in European FIDs in 2025, reaching 9.5GW, with several projects in these countries on track for final approval. Poland in particular is expected to see multiple major wind farms reach FID, including Polenergia and Equinor’s Baltyk II and III, following the recent FID for Orsted and PGE’s Baltica 2 in late January 2025.